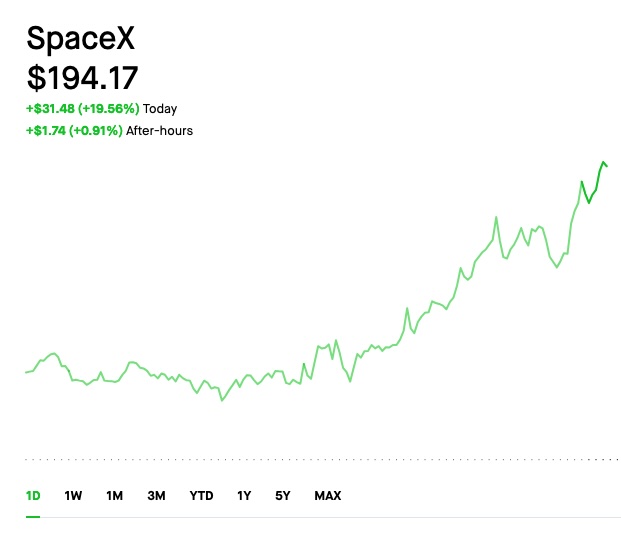

SpaceX’s valuation has surged to a staggering $194 billion, with the company’s total worth reportedly now exceeding $2.52 trillion. But beneath this eye-watering figure lies a more nuanced reality.

Valuation Hinges on Short Position and Debt Payments

The valuation surge is being threatened by a $5 billion short position and the looming specter of a missed debt payment. Specifically, a $183 million debt payment due on June 1 has raised concerns about SpaceX’s liquidity. While a 30-day grace period has been triggered, this still puts pressure on the company’s cash reserves.

As Brian Wang, a well-known futurist and science blogger with a monthly readership of 1 million, notes, this development is not entirely separate from the $5 billion short position. The short position is effectively betting against SpaceX’s valuation, and the missed debt payment has amplified these concerns.

The Role of Echostar in the Valuation

The valuation conversion from SpaceX to Echostar is also a point of contention. The exact details of this conversion are shrouded in secrecy, fueling speculation and uncertainty among investors. This opacity has contributed to the volatility in SpaceX’s valuation, as investors struggle to accurately assess the company’s worth.

What this means

The situation highlights the complex interplay between debt, liquidity, and valuation in the world of space technology. For investors, it’s a stark reminder of the risks involved in riding the SpaceX wave. For SpaceX itself, it serves as a wake-up call to prioritize cash management and debt repayment. The company’s long-term prospects are still bright, but the short-term challenges cannot be ignored.