A recent warning from the Organization for Economic Co-operation and Development (OECD) has sent shockwaves through global markets, with the international body stating that the prolonged conflict in Iran poses a significant threat to the world economy.

Economic Consequences Mount

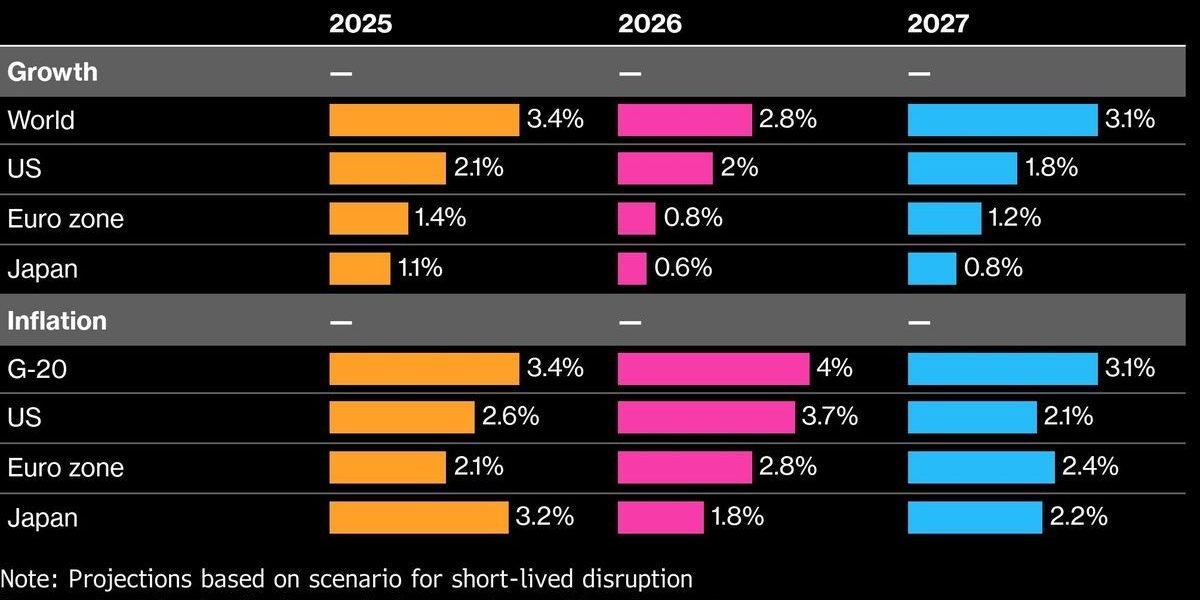

The OECD, a coalition of 38 leading economies, has long been a trusted source for economic analysis. Their latest warning paints a dire picture of a global economy on the brink, with growth stifled and the potential for widespread recession and inflation on the horizon.

At the heart of the OECD’s concerns is the ongoing conflict in Iran, which has already disrupted global oil supplies and sent prices skyrocketing. The ripple effects of this conflict are being felt across the globe, with economies from Europe to Asia struggling to stay afloat in the face of rising energy costs.

According to the OECD, the potential for recession is particularly acute in Europe, where many countries are already struggling to contain inflation and manage their national debt. A recession in this region could have far-reaching consequences, potentially spilling over into other parts of the world and triggering a global economic downturn.

What This Means for You

In practical terms, the OECD’s warning means that consumers and businesses alike should be prepared for a potentially rocky ride ahead. Rising energy costs will likely continue to drive up inflation, making everyday goods and services more expensive and eroding purchasing power.

For those with investments, the warning may also signal a need to reevaluate their portfolios and consider more cautious strategies in the face of economic uncertainty. And for policymakers, the OECD’s warning serves as a stark reminder of the need for swift and decisive action to mitigate the impact of the conflict on the global economy.

OECD’s Forecast: A Delicate Balance

The OECD’s forecast is a delicate one, with the organization warning that the global economy teeters on the brink of disaster. With the conflict in Iran showing no signs of abatement, the OECD’s call to action is clear: policymakers must act swiftly to prevent a global economic downturn.

As the world watches with bated breath, the OECD’s warning serves as a stark reminder of the interconnectedness of the global economy and the potential for seemingly local conflicts to have far-reaching consequences.